Islamic Finance and Dispute Resolution

Article from: TDM 6 (2022), in Editorial

Introduction

The fundamental tenet of Islamic finance is that the expected outcome of such transaction is profit-loss-sharing based (i.e. returns to be linked to risks) as opposed to conventional finance which is interest based. Islam prohibits interest (i.e. riba- the payment of a fixed or determinable interest on funds)[1], hence any transaction based on riba or interest is not allowed in Islamic law or Shari'ah. Islam prohibits not only riba, but also other financial transactions that involve the concept / practice of gharar (deceptive uncertainty, asymmetrical information), maysir (gambling, speculation) and harām (prohibited behaviour). Above all, Islamic finance is geared to social purpose and community welfare, and it is socially inclusive unlike conventional finance. These principles are the drivers of Islamic finance not only on the religious but also on moral grounds.

Since the dawn of Islam, the existence of Islamic finance has been recognised and it has had a long tradition. However, over the last few decades it has been progressively emerging as an alternative finance on the international level as not only many Islamic countries have practised it but many Western banks and financial institutions have sponsored it and made provision for it with the help of their countries' favourable legislative changes. The popularity of Islamic finance appears to be on the rise since the 2008 financial crisis as it is considered by many as a panacea to the ills of conventional finance in many respects.

Even Pope Benedict XVI in his formal Vatican statement advised the Western banks to look out for Islamic finance practice as an ethical model of banking for their salvation from the effect of the meltdown.[2] In that sense, as an ethical business model Islamic banking appears to cross the religious boundaries. It has to be noted that in Europe, during the Middle Ages, the great Catholic theologians propagated against usury. As Thomas Aquinas famously wrote, "to take usury for money lent is unjust in itself, because this is to sell what does not exist and this evidently leads to inequality which is contrary to justice."[3] Similarly, in 1515 Pope Leo X wrote that usury "is not a sin because it is prohibited; rather it is prohibited because it is in itself sinful, for it is contrary to natural justice."[4] It is thus on both moral and religious grounds that usury is prohibited, and there was, in fact, anti-usury law in the European Christendom in the Middle ages.

It has to be acknowledged that Islamic banking principles once guided the trade and financial activities in the Arab Muslim World and the Mediterranean as well as in Spain and the Baltic states, and the system lasted until the 15th century.[5] However, with the rejuvenation of Islamic financing in the Arab World in the 1970s and 1980s[6], the momentum had the rippling effect in both the Muslim world and the non-Muslim world alike. Now, Islamic finance is provided by dedicated Islamic banks and other Islamic finance institutions and also through Islamic windows of conventional banks everywhere. There are about 1500 Islamic financial institutions (still counting) across the globe ranging from retail banks to investment banks and asset managers.

In the post-COVID-19 pandemic era, Islamic finance is increasingly considered as a viable means and option of financing global recovery in the years to come alongside the conventional financing.[7] It has been reported that "(m)ajor financial markets are discovering solid evidence that Islamic finance has already been mainstreamed within the global financial system - and that it has the potential to help address the challenges of ending extreme poverty and boosting shared prosperity."[8] It is also noted lately that "The world currently faces a $15 trillion infrastructure investment gap by 2040."[9] There is no doubt that Islamic finance can contribute to that much needed fund.

The World Bank, the IMF and other international financial institutions are very much enthusiastic about the global prospect of Islamic financing and more specifically for the UN Sustainable Development Goals,[10] not to mention their increasing attention to Islamic financing vehicles over the last decade or so. Even without the prospect of the post-COVID-19 pandemic in sight, the upward trend of Islamic finance was notable. Over the last decade, Islamic finance grew by 10-15 per cent which is far higher than that of conventional finance. It is noteworthy that according to the 2017 ICD-Reuters report[11] global Islamic finance was estimated to be $2.2 trillion of assets in 2016 which rose by the end of 2018 to $2.6 trillion, $2.88 trillion in 2019 and was expected to grow to $3.8 trillion of assets by 2022 and is also forecast lately to stand at $4.95 trillion in 2025.[12] This means that over the decade since 2016 the global Islamic finance will grow more than double.

Let us look at some recent illustrations to appreciate the growth and the hubs of Islamic finance as follows:

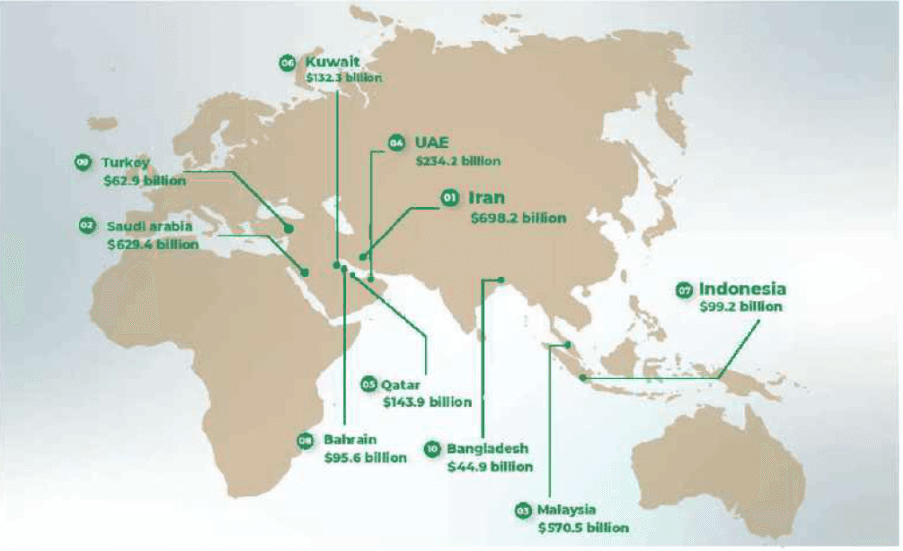

It was elsewhere noted in November 2020 that 10 countries account for almost 95% of the world's shari'ah-compliant assets. Iran leads the way with 29% of the global total followed by Saudi Arabia (25%), Malaysia (11%), the United Arab Emirates (8%), Kuwait (6%), Qatar (6%). Turkey (2.6%), Bangladesh (2.1%), Indonesia (2%) and Bahrain (1.8%).[13] It is reported that "financing by Islamic banks in Pakistan registered a significant 40% annual growth during 2021-2022.[14]

Top 10 Countries by Islamic Finance Assets (2020) [15]

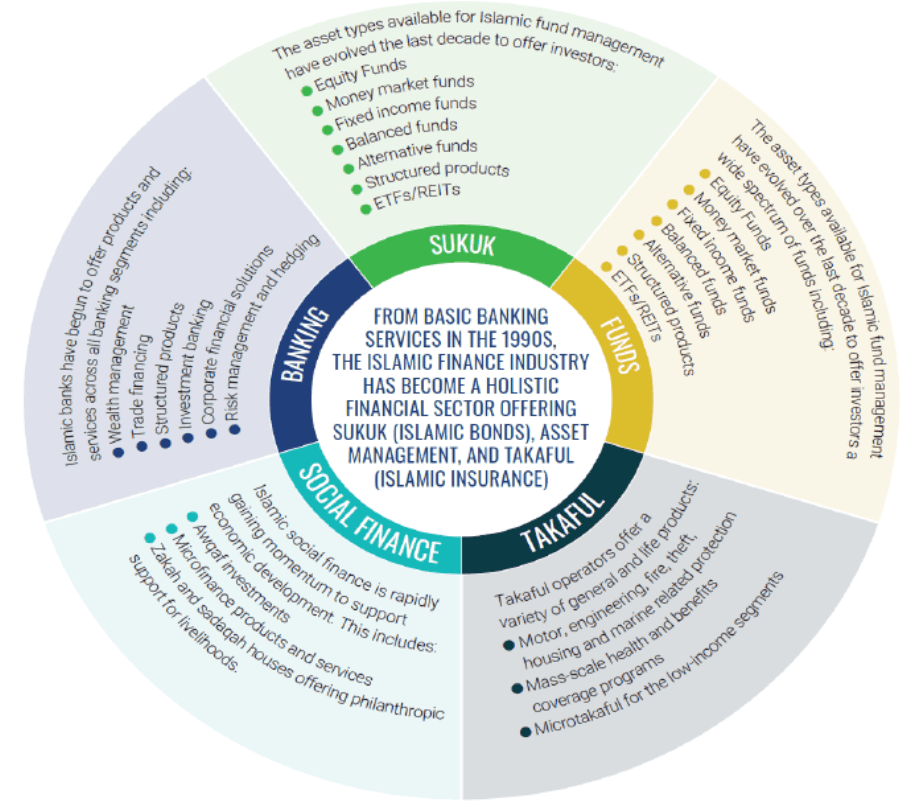

The Islamic finance industry consists of Islamic banking, Islamic capital markets (e.g., sukuk and funds), takaful (Islamic insurance), Islamic microfinance, awqaf (endowments), Zakah and Sadaqah as shown in the following chart.

The Main Sectors of Islamic Finance

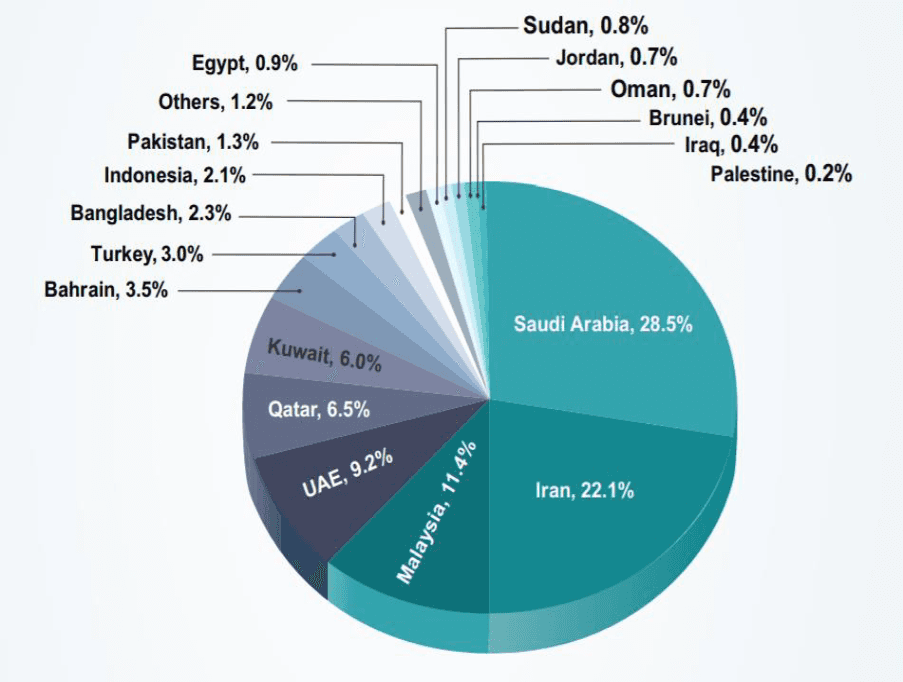

A per the current state of play, in the Islamic finance industry banking is the largest sector comprising both Islamic banks and conventional banks with Islamic windows in both Muslim and non-Muslim countries. The banking sector globally represents 77% of all Islamic financial assets.

Global Islamic Banking Sector (2020)

It is noteworthy that over 50% of the Islamic banking asset is concentrated in two countries such as Saudi Arabia (28.5%) and Iran (22.1%). The other major players are Malaysia (11.4%), the UAE (9.2%), Qatar (6.5%) and Kuwait (6.0%).

It has to be noted that Islamic financial technology (Fintech) has lately proved to be another progressively rapid growth area.[16] In different parts of the world, Fintech is mushrooming consistently. So far, Saudi Islamic Fintech is considered to be the largest worldwide, and it is projected from its current estimate of $17.8 billion to grow to $47.5 billion (a growth of 22 per cent annually) by 2025 in Saudi Arabia[17] with the global projection reaching at $120 billion by the same time. It shows that with the growing computer and online-savvy younger generations (including the marginal ones), especially in the Arab Muslim World, Fintech will exponentially grow "with its tangible traction across multiple markets and jurisdiction" [18] in the years ahead to significantly boost Islamic finance across the globe [19] and thereby the emerging global Islamic economy. [20] It should be noted that the 2013 Sheikh Mohammad bin Rashid Al Maktoum initiative to make 'Dubai as the Capital of the Islamic Economy' added a new dimension to Islamic finance in the region.[21]

It has to be borne in mind that there is no monolithic system of Islamic law to govern Islamic financial transactions.[22] There are different schools of thoughts ( uṣūl al-fiqh ) in Islam. In Sunni Islam, there are four major schools of jurisprudence or fiqh such as the Hanbali School, the Maliki School, the Shafei School and the Hanafi School. Broadly, apart from the matters that can be clearly governed by the Quran and the Sunnah, differences arise as to the other sources of Islamic law or Shari'ah such as ijma (consensus) and qiyas (analogical deduction by reasoning), etc. There are also other schools of jurisprudence in Shia Islam, e.g., Ihna Ashari, or Ja-fari, Ismaili, and Zayadi.

There are also legal systems in Muslim countries which are either a combination of civil law or common law and Islamic law as a hybrid system such as in the UAE, Egypt and Pakistan, etc. This can also add an extra layer of complexity. Given the differences of views, their nature, scope and context on many matters especially in Islamic finance, a unified and harmonised system of Islamic law is increasingly desired across the globe as Islamic finance is gaining the momentum at present.

It has to be acknowledged that the Bahrain-based entity called Accounting and Auditing Organization of Islamic Financial Institutions (AAOIFI)[23] has, as noted, "developed more than 100 standards on Shari'ah law, accounting, auditing, ethics and governance issues for international Islamic finance."[24] Such standardization of the Shari'ah rules is market-driven, responsive to stakeholders' needs and also forward-looking in the context of the ever-developing Islamic financial architecture.[25] In order to facilitate the sustainable growth of Islamic finance around the world, efforts are currently going on in various forums to build a unified global legislative framework for Islamic finance.

The Paris-based International Chamber of Commerce (ICC) has the vision of such a global legal framework for "Islamic Finance through the convergence and codification of Islamic contract law"[26] and legality of various transactional structures and modes under Islamic financing. There is also, according to some views, some urgency, given the fast and steady growth of Islamic finance, in favour of an international treaty to harmonize the laws, standards and practice of Islamic finance across the board.[27] In 2020, the UAE also took an initiative along the lines as it aspires to be the Islamic Financial Hub in the foreseeable future.[28] It is, however, still on the drawing board and the work is in progress.[29] It is noted in a 2022 Report that "(t)he project's stated objectives include providing a global legal benchmark for Islamic finance, reducing regional differences in product offerings and practices, providing legal protection to all parties involved, and developing an international dispute resolution framework."[30] If it comes to fruition, it may pave the way for the building blocks towards the development of a uniform body of law amounting to Islamic lex mercatoria [31] / lex Islamica [32] in the Islamic financial sector across the globe over time. It is notable that to this body of law the jurisprudence or case law of Islamic finance litigation and arbitral tribunals' awards and decisions will progressively contribute to the sustainable growth of Islamic finance globally.

As pointed out above, if such is the upward trend of the growth of Islamic finance[33], there will also be a concomitant growth of disputes between parties in various Islamic finance transactions along the way. A sound dispute resolution system is considered to provide the vehicle for the progressive growth and development of Islamic finance worldwide. Thus, the Islamic finance disputes horizon appears to be a progressive growth area in the foreseeable future for serious consideration by dispute resolution specialists.

Disputes arising out of Islamic finance have been in many cases referred to litigations by the parties involved leading to unsatisfactory outcomes due to the failure of the courts, especially in the Western world, concerned to apply Shari'ah (Islamic law) principles as agreed by the parties in their contract, or due to their misconceptions of Shari'ah.[34] As the popularity of Islamic finance is on the rise in both Islamic and non-Islamic countries, so will be the differences in understanding Shari'ah or Islamic rules and principles applicable to such transactions between diverse parties giving rise to multifarious types of disputes on the international level. Besides, there also arises the debate about the suitability of the various methods of resolution of Islamic finance disputes such as litigation, arbitration, mediation, conciliation, etc.[35] Various other issues relating to Islamic financial disputes may arise.

It has to be noted that arbitration in increasingly considered to be a suitable mechanism for Islamic finance dispute resolution to avoid unpredictable outcomes in litigation in national courts when Shari'ah is in issue due to the courts' attitude to Shari'ah as well as their often misconceptions of Shari'ah as reflected in English court cases concerning Islamic finance, for example.[36] Thus, the International Islamic Financial Market (IIFM) provides for arbitration in its standard documents.[37] There are also other prominent institutions for Islamic dispute resolution which make suitable arbitration rules and adoptable model clauses suitable for such disputes. For example, the International Islamic Mediation & Arbitration Centre (IMAC)'s Shari'a Arbitration Rules, the Asian International Arbitration Centre (AIAC)'s i-Arbitration Rules (2021)[38] and the International Islamic Centre for Reconciliation and Arbitration, i.e. IICRA's revised Arbitration and Reconciliation Rules (December 2020)[39], the revised P.R.I.M.E. Finance Arbitration Rules (January 2022).[40] The Astana International Financial Centre (AIFC), which was officially launched in July 2018, is a prospective venue for disputes arising out of Islamic finance.[41] In a recent report ICC points out the suitability of the ICC Arbitration Rules as it states that the disputes arising out of Islamic finance instruments (as any other dispute involving financial institutions) can be resolved through arbitration and existing rules.[42]

However, it has to be noted that financial dispute resolution requires special expertise. It has been observed that:

"What makes disputes in banking and finance different? After all, like most commercial disputes, their determination often requires the interpretation of contracts, deciding whether a party is liable in contract or tort, and quantifying damages. Furthermore, financial institutions are, in many respects, no different from other commercial parties to disputes. . . Yet, in practice banking and finance disputes require special expertise to resolve them."[43]

This is true more in the context of Islamic finance dispute settlement when Shari'ah is the governing law where an expertise in Islamic law and philosophy is essential.

* * *

Structure and Content

The Special Issue is organised thematically into three parts: Part I, Part II and Part III.

Part I is concerned with the landscape of Islamic finance, in general, in the Organization of Islamic Cooperation (OIC) countries and, in particular, in Bangladesh and Pakistan as two fast-growing Islamic finance hubs. Also, it looks at the trend of Islamic finance in China as a non-OIC country as China's role will be increasingly apparent in the context of its Belt and Road Initiative (BRI) project in its transactional and financial relationships with many Muslim counties where Islamic finance is practised in various degrees.

In their study, Mohieldin and Hamzah have sketched the role of Islamic finance in the post-Covid-19 pandemic era in the Organization of Islamic Cooperation (OIC) countries to meet the sustainable development goals (SGD), given the fact that Islamic finance is gaining rapid growth since the global financial crisis coupled with the adoption of fintech recently[44]. It explains how Islamic finance can create opportunities to increase the global reach of Islamic financial services and enhance financial inclusion.

Hasan's article examines the domestic legal framework of Sukuk in Bangladesh to check its compatibility with the international standards, especially with the Malaysian regime (another major Islamic finance-hub OIC country). It considers the prospects of Sukuk in Bangladesh and outlines the challenges and limitations of the Sukuk market there. It also examines the loopholes in the existing regulations in Bangladesh and suggests for improvements using the Malaysian regime as a model.

Piracha's article is focused on the Islamic Republic of Pakistan as a rapidly rising OIC Islamic economy to explore its philosophy, theory and practice regarding banking and finance which could prove to be a test case for many other growing OIC Islamic economies. It provides insights into the evolution of the legal framework in Pakistan pertaining to Islamic finance and its inconsistency with the international legal regime of Islamic finance.

China is an emerging leading economy and its Belt and Road initiative (covering many Middle Eastern countries and non-Arab Muslim states) will have significant relevance to Islamic finance transactions in its dealing with those countries in the years to come. Erie's article explores the prospect of Islamic finance in China's transactional relationship with many Muslim countries where Islamic finance principles are more often than not the norm. Thus, Chinese commercial and financial institutions will experience a learning curve. It reviews the short history of Islamic banking in China, assesses the current supply of Shari'ah-compliant financial instruments for cross-border business between Chinese parties and their counterparts based in Muslim states, appraises the demand of Chinese enterprises for Islamic banking products and services, and, lastly, suggests possible trajectories for the integration of Islamic finance into the political economy of China and Muslim states.

Part II looks at the jurisprudence and the law applicable to Islamic finance and disputes.

In his paper Wahab aims at disambiguating the doctrine of Al-Maqāsid Al-Shar'īyah (objectives/aims of Islamic law) as a fundamental concept of Islamic law and finance and also analyses some of the general legal maxims and jurisprudential principles of Sharī'ah law. The importance of the doctrine of Al-Maqāsid Al-Shar'īyah and the jurisprudential principles of Sharī'ah law transcends the boundaries of Islamic finance transactions and represents a fundamental tenet that guides any conducive Ijtihad (diligent research) across all aspects of Islamic law. This doctrine defines the philosophy underlying Islamic norms and principles and is undoubtedly crucial for arbitral tribunals when confronted with questions of Islamic Sharī'ah and when asked to make determinations based on applicable Islamic legal principles.

Nosrollah Ebrahimi and Mahdi Ebrahimi's paper is focused on the methods of Islamic finance dispute resolution in Iran and also the Shi'a jurisprudence that may be applicable in Iran to Islamic finance and dispute resolution as a Shi'a Muslim dominated major country. Having discussed the different methods of Islamic finance dispute resolution such as mediation, med-arb, arbitration and litigation as are practised in Iran, it turns to emphasize the most important underlying factor for any kind of sound Islamic finance dispute mechanism, i.e. the quality of the knowledge and the level of expertise and experiences of the individual or group of dispute resolvers or board of disputes settlement/adjudication to resolve such disputes. In their view, the expertise of such dispute resolvers needs to be at the level of ijtihad in order to be able to appreciate both the technical side of Islamic finance as well as the application of Shari'ah or Islamic law to it especially from the perspectives of the Shi'a jurisprudence as is applicable in Iran. They particularly advocate that while settling Islamic finance disputes particular attention should be given to the established Islamic jurisprudential principles namely principles of La-zara va la zerar ("no harm and no loss"), principle of solteh-e-motlaqeh ("despotic dominion"), principle of dhaman-e-ghahri (non-contractual in the meaning of civil liability), principle of tasbib (causation) and principle of itlaf (dissipation).

Tavana 's paper addresses the issue of Shari'ah as the applicable law to Islamic finance disputes in two parts. In the first part, the challenges when Shari'ah is chosen as the applicable law as are spotted in light of the available case law from the English courts. The second part provides a proper solution to those challenges by proposing the application of the principles of Shari'ah concerning commercial transactions together with a complementary law.

Zahid's article concerns the choice of law and choice of forum (belonging to an Islamic jurisdiction) in the context of an international commercial / financial contract from an Islamic law perspective. He makes a theoretical inquiry into the matter in respect of a single choice of law that conflicts with Shari'ah law in full or part and also in respect of a combined conflicting choice and the forum's attitude to that. Secondly, he looks at the scenario in the case of a single choice of Shari'ah law and ponders over the issue of the forum's jurisprudential approach or the prospect of the school of fiqh (madhhab) to follow.

Abid's article explores the practical aspects of Islamic project finance, notably, aspects that largely set the Islamic project finance apart from the conventional project finance, in addition to the main challenges facing the use of Islamic project finance at a larger scale. This article is structured in three main sections: the first section briefly describes conventional project prevalent in project financing, the second section lays down a number of Islamic finance techniques and the third section analyses a number of challenges facing Islamic project finance structures. It also looks at the issues of mingling Islamic funds with other non-Islamic funds in multi-sourced projects throughout.

Part III includes an array of articles dealing with Islamic finance dispute resolution, Islamic versus conventional finance dispute resolution, dispute resolution methods, some procedural aspects including some characteristics of Islamic finance dispute resolution and some institutions. The thrust of this part is to identify some trends and explore them in respect of the aforementioned aspects rather than focusing comprehensively on them.

Islamic finance disputes have traditionally been subject to litigation in the hubs of common law systems such as London and New York more than to international arbitration. Connerty's article looks at Islamic finance disputes through the lenses of an English lawyer in litigations in London and New York. It also considers arbitration as a method of Islamic finance dispute resolution. Finally, it considers the recognition and enforcement of such arbitral awards under the New York Convention.

Tsaturya's paper attempts to provide an overview of the Islamic financial instruments, which conform to Shari'ah law and, based on their specifications, explore the suitability of litigation, arbitration and other methods of alternative dispute resolution for resolving disputes involving these instruments.

Mahmood, Juss and Dowling-Hussey's article looks at the under-explored method of Islamic dispute resolution (IDR) alongside the conventional alternative dispute resolution ('ADR') method. It emphasizes that a comprehensive understanding of the two would well equip one to work out IDR better.

Blanke's article explores the case for semi-secular arbitration as a viable form of dispute resolution in the Islamic finance industry and also confirms the procedural and commercial viability of the same. It is considered that semi-secular arbitration will allow disputing parties to mitigate the Shari'ah risk by facilitating Shari'ah compliant dispute resolution in a forum that is acceptable and accessible to non-Muslim investors without placing them at a perceived procedural disadvantage whilst providing the comfort of a Shari'ah compliant outcome.

Alrefaei 's paper sketches the current state of the arrangements of Islamic finance dispute resolution in Saudi Arabia, a country at the forefront of Islamic finance system in the world. It indicates that with the ever-increasing role of Islamic finance in the Islamic economy and beyond, and Saudi Arabia, being in the leading role, should embrace arbitration as a method of Islamic dispute resolution and it will be along the lines of the aspirations of the Kingdom's Vision 2030.

Bantekas examines the following matters in his article: a) Islamic law as the governing law of contracts; b) the absence of a distinct Islamic arbitral process, as such: c) the relative conformity of public policy exceptions with industrialized arbitration-friendly states and; d) whether there is a need for a global hub for Islamic finance arbitration, with particular emphasis on the Qatar Financial Center (QFC) and its specialized court. He endeavours to show that there is no reason to fear the secularization of the Islamic finance arbitration's essential elements by the referral of disputes to secular arbitral institutions.

The remaining three articles deal with three disparate issues in the context of Islamic dispute resolution such as the prohibition of riba in awarding in post-award interest in international arbitration, the role of Shari'ah Advisory Council (SAC) in Islamic dispute resolution in Malaysia and the prospect of third-party funding within the Islamic framework.

Nodoushan and Jahangard's article discusses the impact of the prohibition of riba (interest) under Shari'ah on the ability of dispute settlement body (in particular an arbitral tribunal) to award post-award interest and on the enforcement of such awards in those Islamic countries that their legal systems are strongly influenced by principles of Shari'ah. It argues that this problem can be solved by issuing an award on specific performance combined with an award on liquidated damages for late/non- compliance with the arbitration award.

Zain and Hasan's article looks at the important role of the Shari'ah Advisory Council (SAC) as a strategy for better dispute settlement in the Islamic financial services industry in Malaysia. It has adopted qualitative and doctrinal legal methodologies to trace the crucial role of SAC in the dispute settlement process in the Malaysian regulatory framework. It has found that the involvement of SAC in the process of dispute settlement is a unique legal innovation adopted in Malaysia and it could be a model for other jurisdictions.

Can's article examines the suitability of third-party funding (TPF) in Islamic finance disputes. He views that since Islamic finance transactions are based on profit-loss sharing rather than interest akin to the practice of TPF and it is expected to fit very well into the framework of Islamic law. In his doctrinal analysis he concludes that TPF as a financial tool within Islamic finance is indeed in accordance with Shari'ah Law. In his analytical approach he looks at the compatibility of TPF in each of the seven major schools of Shari'ah Law, including four Sunni doctrines (i.e., Hanbali, Maliki, Shafi'i and Hanafi) and three Shia doctrines (i.e., Isna Ashari, or Ja-fari, Ismaili, and Zayadi). He considers TPF as a new vision within the context of Islamic jurisdictions, particularly in Shari'ah, and highlights the significance of a developing funding market like TPF which makes the judicial system and justice accessible to many what may not be the case otherwise.

Footnotes

[1] Although the very notion of the prohibition of riba is well acknowledged, the nature, scope and the context could be sometimes subject to controversy. See Filippo di Mauro, et al, "Islamic Finance in Europe", available at: https://www.ecb.europa.eu/pub/pdf/scpops/ecbocp146.pdf . See also, Ibrahim Shehata, "Partial Refusal to Enforce Award Brings Out Interest Rates Public Policy Dilemma", ICC Dispute Resolution Bulletin (2020, Issue no.2), p.55; S. Singh, "The Mirage of Interest-Free Islamic Finance" (May 22, 2021), available at: https://www.linkedin.com/pulse/mirage-interest-free-islamic-finance-sukudhew-sukhdave-singh/; S. Aren, & H.N. Hamamci, "The mediating effect of religiosity in evaluating individual cultural values regarding interest. 9 Turkish Journal of Islamic Economics", (2022, no.2), 73-97; Available at: https://www.tujise.org/content/7-issues/19-9-2/a2881/tuj2881.pdf H.A. Hamoudi, "The Muezzin's call and the Dow Jones Bell: on the necessity of realism in the study of Islamic law" 56 The American Journal of Comparative law (2008, no.2) 423; See Historic Judgment on Riba, available at: https://old.ethica.institute/Historic-Judgement-On-Riba.pdf; Chibli Mallat, The Debate on Riba and Interest in Twentieth Century Jurisprudence, in Islamic Law and Finance (1988); Mahmoud Amin El-Gamal, "Interest and the Paradox of the Contemporary Islamic Law and Finance", 27 Fordham Int'l L.J. (2003, no.1), 108. See for some detailed discussion in Mahmood Hussain Ali Ahmad, "Critical Study of the Role of Sharia Public Policy in the Recognition and Enforcement of Foreign Arbitral Awards in UAE" (unpublished PhD thesis, 2020, University of East Anglia, U.K.), esp. Chapter 4.

[2] See: available at: https://www.worldfinance.com/news/vatican-praises-ethical-sharia-banking.

[3] Quoted in J. Arthur Bloom, "Sharia Law: As American As Apple Pie", available at: https://dailycaller.com/2019/04/15/sharia-law-american-apple-pie/.

[4] Ibid.

[5] See https://mfr.mv/islamic-finance/overview-islamic-finance-in-the-maldives.

[6] M. Priest and R. Wilson, "Finance In The Arab World: Resurgence of old ideas about handling cash", The Times, London, 6 March 1981; M. Hussain, A. Shahmoradi, and R. Turk "An Overview of Islamic Finance" 2015, IMF Working Paper WP/15/120, International Monetary Fund, Washington D.C.

[7] See Islamic Finance Outlook (2022 edition), available here: https://www.spglobal.com/ratings/en/research/pdf-articles/islamic-finance-outlook-2022-28102022v1.pdf. It notes: "S&P Global Ratings believes the global Islamic finance industry will expand 10%-12% in 2021-2022. The expansion of Islamic banking assets in some Gulf Cooperation Council (GCC) countries, Malaysia, and Turkey and sukuk issuances exceeding maturities explain this expected performance. Islamic finance expanded rapidly in 2020 with total assets increasing 10.6% despite the double shock from the COVID-19 pandemic and drop oil prices."

[8] See https://www.worldbank.org/en/programs/global-islamic-finance-development-center.

[9] See https://www.refinitiv.com/en/infrastructure-investing. See also The Sustainable Infrastructure Investment Report - Potholes on the Road to Sustainable Infrastructure: Exploring the Trends, Participants and Data Powering a Sustainable Infrastructure Boom. Available at: https://www.refinitiv.com/en/infrastructure-investing/insights/sustainable-infrastructure.

[10] See "How Islamic Finance Contributes to Achieving the Sustainable Development Goals" (OECD Development Policy Papers, June 2020, No.30), available at: https://www.sdgphilanthropy.org/system/files/2020-07/OECD_Islamic%20Finance.pdf. See also E. Richardson, "The UAE and Responsible Finance-Can Responsible Finance Ṣukūk Help the UAE in Fulfilling Its Sustainability Ambitions?", 34 Arab Law Quarterly, (2020, no. 4), 313-355: https://brill.com/view/journals/alq/34/4/article-p313_1.xml.

[11] Available at: https://islamicbankers.files.wordpress.com/2017/12/icd-thomson-reuters-islamic-finance-development-report-2017.pdf.

[12] See news report: Salaam Gateway, available at: https://www.salaamgateway.com/story/newswrap-islamic-finance-2-3-4-5-6-7-8-9-10-11-12-13-14.

[13] See https://www.gfmag.com/topics/blogs/islamic-finance-just-muslim-majority-nations.

[14] State Bank of Pakistan - Islamic Banking Bulletin (April - June 2022), available at https://www.sbp.org.pk/ibd/bulletin/2022/Jun.pdf.

[15] ADR Islamic Economy - Bulletin of the International Islamic Centre for Reconciliation and Arbitration (2022, Issue No.19), p.9.

[16] See Islamic Finance Outlook (2022 edition), available here: https://www.spglobal.com/ratings/en/research/pdf-articles/islamic-finance-outlook-2022-28102022v1.pdf.

[17] See Arab News: https://arab.news/bwmuq.

[18] Sayed Farooq, "10 years on: what's next for the global Islamic economy" (Salaam Gateway, 8 June 2022), available at: https://salaamgateway.com/story/10-years-on-whats-next-for-the-global-islamic-economy.

[19] It is noted that Sharia-compliant fintech is poised for explosive growth across both Islamic and western jurisdictions with Refinitiv expecting the market to reach $4.9 trillion within three years. See Salaam Gateway (26 May 2022). Available at: https://salaamgateway.com/story/fintech-promises-to-open-up-global-islamic-finance-markets.

[20] See State of the Global Islamic Economy 2022 Report (Salaam Gateway). Available at: https://salaamgateway.com/specialcoverage/SGIE22.

[21] https://www.emirates247.com/news/dubai-world-capital-of-islamic-economy-initiative-unveiled-2013-10-05-1.523457.

[22] See Horacio A. Grigera Naón and Paul E. Mason, eds., International Commercial Arbitration Practice: 21stCentury Perspectives (2021, Mathew Bender, Lexis Nexis), CHAPTER 3 Shari'a Law Approaches to Arbitration, by Arif Hyder Ali & Ali Ehsassi: https://store.lexisnexis.com/products/international-commercial-arbitration-practice-21st-century-perspectives-skuusSku13400336.

[23] See http://aaoifi.com/?lang=en.

[24] See H. Hasem, et al, "International Standards and Tribunals Being Developed to Solve Islamic Finance Disputes", (Salaam Gateway, 12 July 2022), https://salaamgateway.com/story/international-standards-and-tribunals-being-developed-to-solve-global-islamic-finance-disputes. See Adoption of AAOIFI Standards, AAOIFI, http://aaoifi.com/adoption-of-aaoifi-standards/?lang=en.

[25] J. Ercanbrack, "The Standardization of Islamic Financial Law: Lawmaking in Modern Financial Markets", 67 The American Journal of Comparative Law (2020), p.825.

[26] Commission on Arbitration and ADR, ICC Commission Report: Financial Institutions and International Arbitration 18 (Mar. 2018), https://iccwbo.org/content/uploads/sites/3/2016/11/icc-financial-institutions-and-international-arbitration-icc-arbitration-adr-commission-report.pdf.

[27] Hakimah Yaacob, Marjan Mohammad, & Edib Smolo, International Convention for Islamic Finance: Towards a Standardisation. https://www.researchgate.net/publication/333118798_International_Convention_for_Islamic_Finance_Towards_a_Standardisation.

[28] See https://www.mediaoffice.ae/news/2020/May/06-05/UAE-Launches-Initiative-to-Build-Unified-Global-Legislative-Framework-for-Islamic-Finance.

[29] See Islamic Financial Outlook (2022 edition), available at: https://www.spglobal.com/ratings/en/research/pdf-articles/islamic-finance-outlook-2022-28102022v1.pdf. The Report states: "Over the next 12 months, we expect some progress on the unified global legal and regulatory framework for Islamic finance that the Dubai Islamic Economy Development Centre (DIEDC) and its partners are developing. DIEDC embarked on this project with the Islamic Development Bank, the United Arab Emirates Ministry of Finance, and several other advisors in 2020."

[30] Ibid.

[31] See Kilian Bälz, "Sharia Risk? How Islamic Finance Has Transformed Islamic Contract Law" (Occasional Publications 9, September 2008, Islamic Legal Studies Program, Harvard Law School) p.26.

[32] See https://lexislamica.com/index.php/2019/11/02/introduction-to-islamic-law-as-international-law/.

[33] Asian Development Bank https://www.adb.org/what-we-do/sectors/finance/islamic-finance .

[34] See the English Court decisions Beximco Pharmaceuticals Ltd, Bangladesh Export Import Co. Ltd., Mr. Ahmad Solail Fasiuhur Rahman, Beximco (Holdings) Ltd. v. Shamil Bank of Bahrain E.C.[2004] EWCA Civ 19; Investment Dar Co KSCC v Blom Development Bank Sal[2009] EWHC 3545; Bank Islam Malaysia Bhd v Azhar Osman & Other Cases [2010] 5 CLJ 54 [2010] 1 LNS 251; and Cameron Partners L.P. v. Louisiana Offshore Holding LLC & Ors[2009].

[35] For example, see Farouq Saber Al-Shibli, "Litigation or Arbitration for Resolving Islamic Banking Disputes", 32 Arab Law Quarterly (no.4, 2018), p.413. Available here: https://www.jstor.org/stable/27073515.

[36] See above (footnote 34).

[37] Sukuk Template Prospectus, Sukuk Template Sale and Substitution Undertaking.

[38] Available at: https://admin.aiac.world/uploads/ckupload/ckupload_20211101035047_27.pdf.

[39] Available at: https://www.iicra.com/arbitration/#arbitration-rules.

[40] Available at: https://primefinancedisputes.org/page/p-r-i-m-e-finance-arbitration-rules.

[41] Art. 2 AIFC Constitutional Statute. See Nicolás Zambrana-Tévar, "The Court of the Astana International Financial Center in the Wake of its Predecessors", Erasmus Law Review (September, 2019, Issue no.1). Available at: http://www.erasmuslawreview.nl/tijdschrift/ELR/2019/1/ELR-D-18-00027.

[42] ICC Commission Report: Financial Institutions and International Arbitration (March 2018) para 117. Available at: https://iccwbo.org/content/uploads/sites/3/2016/11/icc-financial-institutions-and-international-arbitration-icc-arbitration-adr-commission-report.pdf.

[43] Georges Affaki, 'Revamping of P.R.I.M.E. Finance Arbitration Rules Underway' Kluwer Arbitration Blog, January 20 2021 http://arbitrationblog.kluwerarbitration.com/2021/01/20/revamping-of-p-r-i-m-e-finance-arbitration-rules-underway/; See also, Arif H. Ali and David L. Attanasio, International Investment Protection of Global Banking and Finance: Legal Principles and Arbitral Practice (Wolters Kluwer, 2021).

[44] See Global Islamic Fintech Report (2022), available at: https://salaamgateway.com/reports/global-islamic-fintech-report-2022.